According to the Commerce Department’s Census Bureau, single-family housing starts fell to a seasonally-adjusted annual rate of 993,000, down 8.4% from December and 0.7% from January 2024. While this most recent month-over-month decline was particularly pronounced—the December-to-January decline in starts has averaged just 0.5% over the past decade—much of it can be attributed to weather-related disruptions. Indeed, December saw an uptick in activity as delayed construction from Hurricane Helene in the fall pushed some projects to later in the year; meanwhile, unexpectedly frigid temperatures in January slowed work across multiple regions.

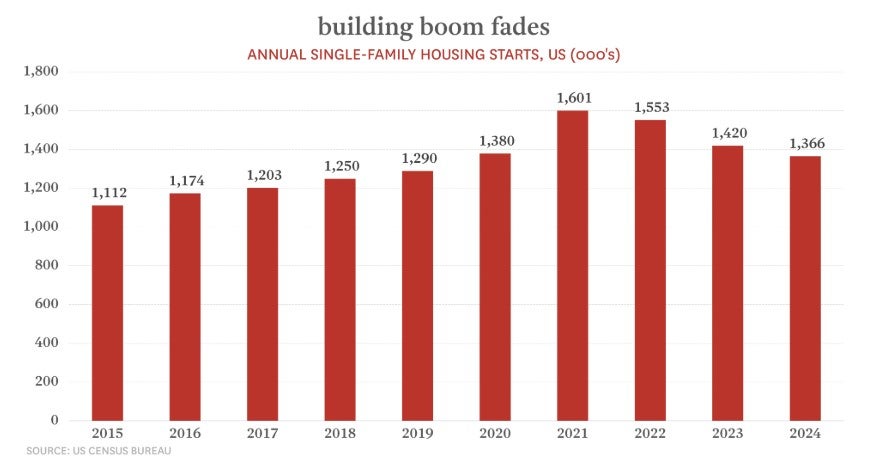

Beyond seasonal fluctuations, the latest figures highlight the broader trends in new home construction. Homebuilding activity has now declined each year since reaching an all-time high in 2021.

Annual housing starts peaked during the pandemic era amid a housing boom fueled by historically-low borrowing costs and shifts in remote work. Since then, housing starts have declined in three consecutive years but remain above pre-pandemic averages. In 2024, they were still 13.3% above the five-year pre-pandemic average (2015-2019).

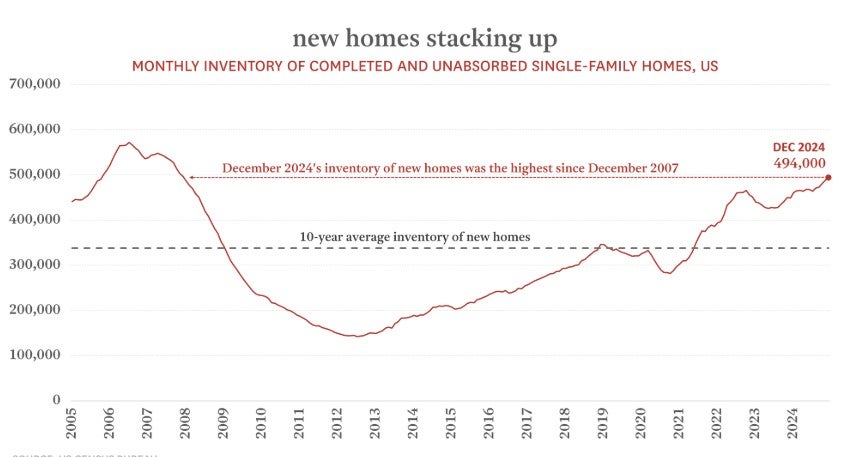

That momentum has left its mark, with the supply of newly-built and unabsorbed homes now at its highest level since 2007.

A closer look at months-of-inventory (MOI)—which tracks how long it would take to sell the current supply of unsold homes at the existing pace of absorbtion—provides more context. While January’s MOI for newly-built single-family homes remains elevated, up 34.9% above the 10-year average, it’s still below the peaks seen during the pandemic.

With supply trending higher but not yet overwhelming the market, homebuilders are likely to adopt a more measured approach in the coming months. Rising inventory levels will factor into project decisions, especially in markets where unsold homes are accumulating.

At the same time, cost pressures remain a challenge. A 10% tariff on all goods coming from China, and a 25% tariff on all steel and aluminum imports are weighing on the construction industry, which heavily relies on imported materials. For example, roughly 30% of softwood lumber used in residential construction comes from international trade. Meanwhile, after some easing late last year, mortgage rates have climbed again, now hovering just below 7% and negatively impacting buyer demand.

January’s data reinforces what’s been true for some time—homebuilders aren’t pressing the brakes entirely, but they’re certainly tapping them.

That momentum has left its mark, with the supply of newly-built and unabsorbed homes now at its highest level since 2007.

A closer look at months-of-inventory (MOI)—which tracks how long it would take to sell the current supply of unsold homes at the existing pace of absorbtion—provides more context. While January’s MOI for newly-built single-family homes remains elevated, up 34.9% above the 10-year average, it’s still below the peaks seen during the pandemic.

With supply trending higher but not yet overwhelming the market, homebuilders are likely to adopt a more measured approach in the coming months. Rising inventory levels will factor into project decisions, especially in markets where unsold homes are accumulating.

At the same time, cost pressures remain a challenge. A 10% tariff on all goods coming from China, and a 25% tariff on all steel and aluminum imports are weighing on the construction industry, which heavily relies on imported materials. For example, roughly 30% of softwood lumber used in residential construction comes from international trade. Meanwhile, after some easing late last year, mortgage rates have climbed again, now hovering just below 7% and negatively impacting buyer demand.

January’s data reinforces what’s been true for some time—homebuilders aren’t pressing the brakes entirely, but they’re certainly tapping them.