But just how much have homebuyers changed, and what does it mean for the housing market? Here, we explore the latest data from the National Association of Realtors, which revealed three record-breaking firsts.

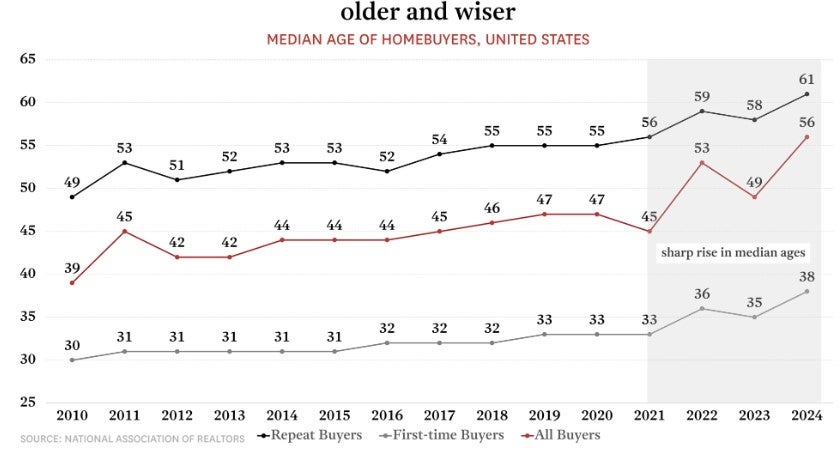

1. Homebuyers are older and earning more than ever before.

In 2024, the median age of homebuyers hit a new high. First-time buyers now have a median age of 38, up from 35 just a year ago. For repeat buyers, the median has risen from 58 to 61.

The pace of this shift has accelerated: while the median age of all homebuyers rose 20.5% over the decade from 2010 to 2020, it jumped 24.4% in just three years between 2021 and 2024.

At the same time, the average homebuyer is also earning significantly more income. Since 2022, the median annual income of homebuyers has risen from $88,000 to $108,000—a 22.7% increase in just two years. For comparison, the Census Bureau reports that the median US household income grew by only 4% over the same period. Historically, homebuyers have earned more than the typical household, but the gap has widened.

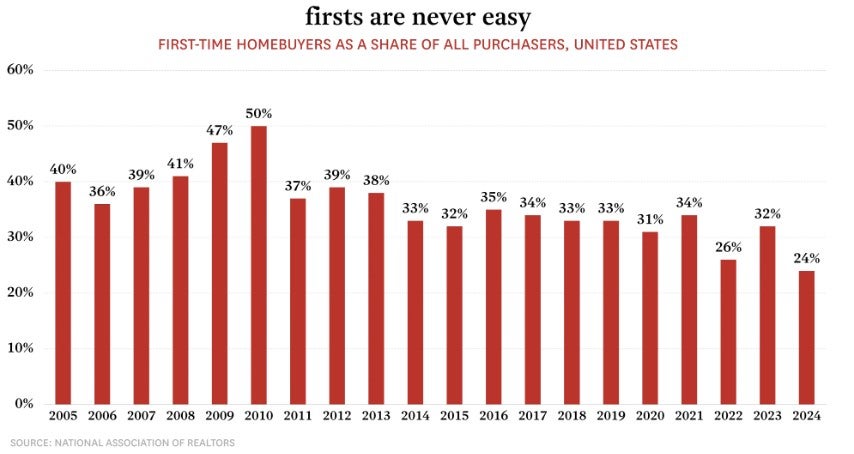

2. First-time buyers are struggling to get their foot in the door—literally.

The number of first-time homebuyers as a share of all purchasers has dropped significantly. Over the past two decades, they’ve made up about 36% of the market, but by January 2025, that figure had dropped to 28%. In 2024, first-time buyers accounted for just 24% of all purchases—the lowest share ever recorded. Unlike existing homeowners—who can leverage existing equity—first-time buyers are absorbing the full impact of today’s costlier housing environment, facing higher mortgage rates, larger down payment requirements, and steeper monthly costs without the financial cushion of a previous home sale.

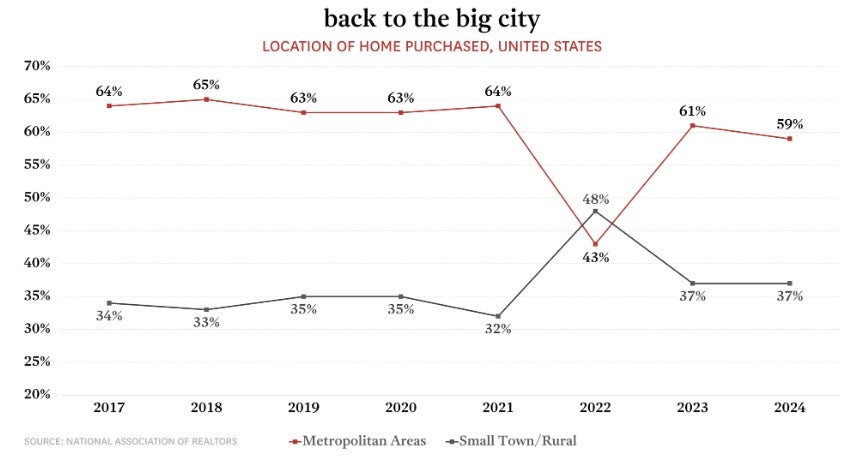

3. Buyers are gravitating toward different types of homes, from urban spaces to multi-generational living.

City living is making a comeback after pandemic-era trends pushed buyers toward smaller towns and rural areas. In 2022, the share of homes purchased in metropolitan areas—regions with a population of 50,000 or more, including both urban cores and suburbs—fell from 64% to 43%, dropping below the share of homes bought in small towns and rural areas for the first time. Since then, purchases in metropolitan areas have rebounded to near long-term averages, with home purchases in urban cores in particular reaching a record high of 16% in 2024.

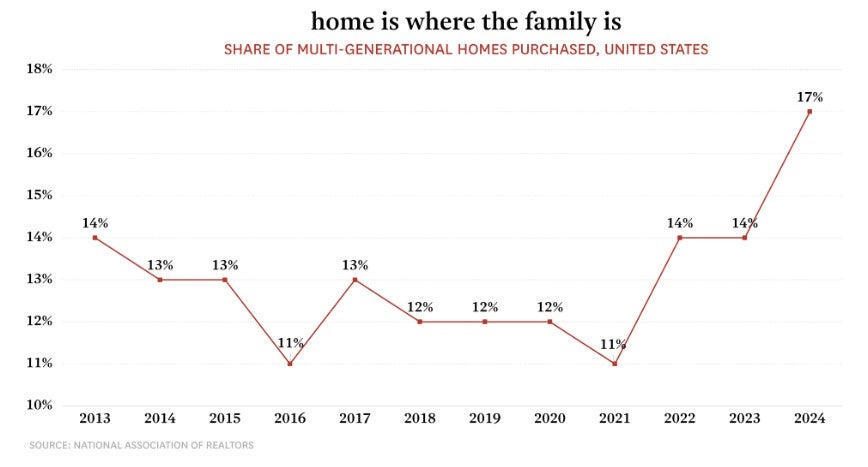

Another notable shift is that more homebuyers are embracing multi-generational living. In 2024, 17% of homebuyers purchased a home shared with adult siblings, grown children, or grandparents—up from 14% in 2023 and the highest share ever recorded. For most, the decision came down to finances, with 57% citing cost savings as a key factor.

The profile of today’s homebuyers has changed in just a few years: they’re older, earning more, and making different choices about where they live. These shifts aren’t just statistics—they reflect deeper changes in who can buy, where they’re buying, and what kind of housing is in demand, and they’re likely to continue to shape the market in the months and years ahead.