Price pressures through much of the CPI eased in November, with the food, shelter, household operations, health and personal care, and alcoholic beverages, tobacco, and cannabis components of the CPI all decreasing in their respective rates of growth last month.

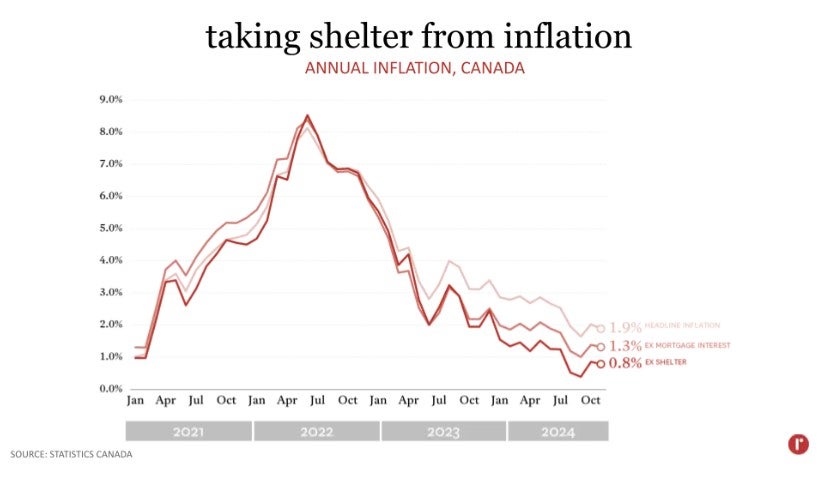

If shelter—which comprises approximately 30% of the CPI–is excluded, aggregate prices for all other goods and services only rose by 0.8% in November, year-over-year.

Notably, the rent component of the shelter category is currently playing an outsized role in driving shelter inflation, with annual CPI rents increasing by 7.7% in November—up from 7.3% in October. That said, these CPI rent increases exceed those presented in the newly-released CMHC Rental Market Report, which indicates that average (purpose-built) rents in Canada increased only 5.4% between October 2023 and October 2024. Most compellingly, neither of these measures reflects the declines observed in asking rents in Canada’s major markets.

The November inflation release likely does nothing to alter the Bank of Canada’s trajectory for monetary policy. Price pressures continue to ease overall, while the labour market has been relatively weak. Before the next Bank of Canada announcement on January 29th, there is both another CPI and Labour Survey release that will be taken into consideration. Based on what we know today, however, a 25-point cut in the Bank’s policy interest rate is likely next month.

The November inflation release likely does nothing to alter the Bank of Canada’s trajectory for monetary policy. Price pressures continue to ease overall, while the labour market has been relatively weak. Before the next Bank of Canada announcement on January 29th, there is both another CPI and Labour Survey release that will be taken into consideration. Based on what we know today, however, a 25-point cut in the Bank’s policy interest rate is likely next month.