Any doubts about whether or not the Bank of Canada will cut its policy rate by a further 25 bps on September 4th were laid to rest this morning with the release of the latest batch of employment data by Statistics Canada.

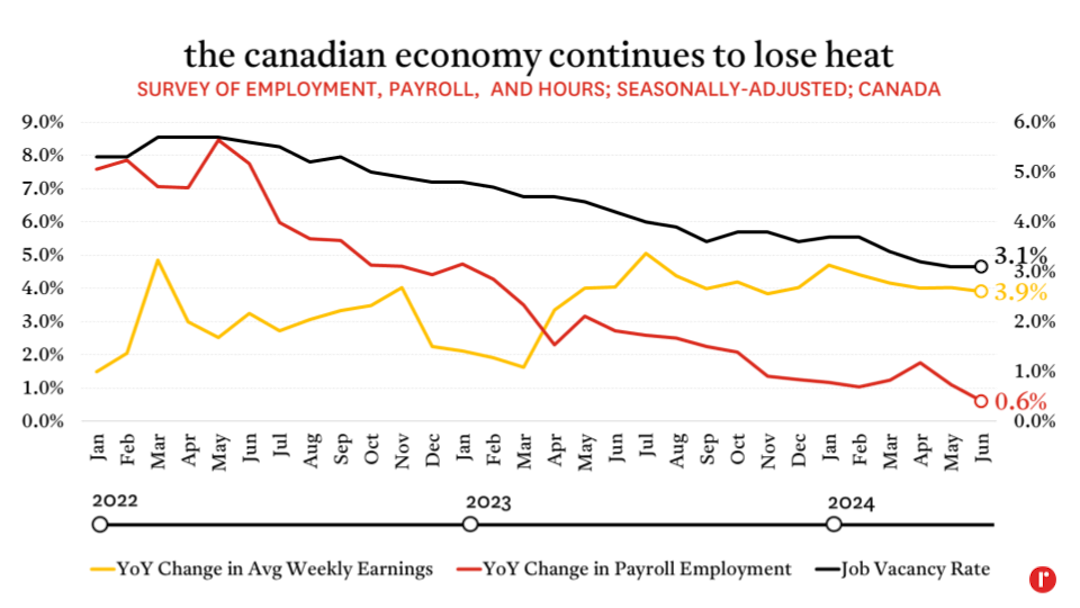

In a nutshell, Canada’s economy continues to underwhelm (as we’ve noted here and here…and here), with the Survey of Employment, Payrolls, and Hours revealing that, on a seasonally-adjusted basis, the country lost 47,253 jobs in June—the largest such decline since 62,772 jobs were shed in November of last year. This pushed the year-over-year gain in jobs in June to a paltry 0.3%, which is the slowest growth recorded since the onset of the pandemic, and the slowest non-pandemic-related change in employment since June 2010.

Meanwhile, the job vacancy rate—the proportion of all jobs (and would-be jobs) that are unfilled—remained at its lowest level (3.1%) going back to March 2020. If it wasn’t already abundantly clear, it is now: the broad-based labour shortages that existed in the wake of the pandemic (when the job vacancy rate peaked at 5.7% as late as May 2022) are a thing of the past. Indeed, the current vacancy rate is on par with the average seen between March 2017 and March 2020.

Wages continue to buck other labour market trends, with the year-over-year gain in average weekly earnings (for both salaried and hourly employees) rising at a 3.9% clip in June—50% faster than the average of the March 2017 to March 2020 period, but down from both 4.0% in May and its post-pandemic peak of 5.1% in July 2023. As inflation moderates (it currently sits at 2.5%), this is a good thing for workers, but also something for the central bank to keep its eye on as it adjusts monetary policy.

On this latter point, currently-elevated earnings growth isn’t sufficient, on its own, to dull the Bank of Canada’s desire to lower borrowing costs, which we expect it to do at least twice over the course of its three remaining meetings in 2024.